Financial information as of 30 September 2018 [1]

Consolidated revenue including the full consolidation of TAV Airports and Airport International Group (AIG) was up by 29.2%, i.e. +€757 million, at €3,353 million.

Excluding the full consolidation of TAV Airports since July 2017, and AIG since April 2018, consolidated revenue was up by 3.6%, at €2,335 million.

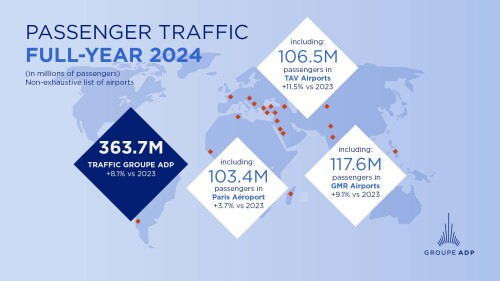

- Groupe ADP's passengers traffic [2] : +8.8%, at 217.6 million passengers over the first 9 months of 2018 (vs. 200.0 million passengers over the same period in 2017).

- Paris Aéroport's traffic [3] : +3.4%, at 80.0 million passengers (vs. 77.3 million passengers over the first 9 months of 2017), thanks to the dynamism of low-cost companies (+10.2%) and international traffic (+5.6%).

-

Aviation activities (+3.6%): growth in airport fees (+5.2%, at €842 million).

-

Retail and services (+5.1%): good dynamics of retail activities (+4.9%, at €359 million), driven by the results of airside shops (+3.9%) and bars & restaurants (+15.4%). Stable sales/pax [4] over the first 9 months of 2018 (€17.8) compared to the first 9 months of 2017, duty free performances being impacted by the works in terminal 2E and strong Euro.

-

Real Estate (+5.2%): increase notably thanks to the positive effect of the full acquisition of the "Dôme" building, in Paris-Charles de Gaulle in December 2017.

-

International and international developments: revenue reflected TAV Airports' results, fully consolidated since July 2017, up to €893 million over the first 9 months of 2018 and AIG's results, since April 2018, up to €125 million.

-

Other activities (-36,4%): decrease linked to the change in Hub Safe consolidation method since September 2017, formerly fully consolidated and now accounted for as share of results from non-operation associates

Groupe ADP revenue by segment for the first 9 months of 2018

|

(in millions of euros) |

9M 2018 |

9M 2017 |

2018 / 2017 |

|

|

Revenue |

3,353 |

2,596 |

+€757m |

+29.2% |

|

Aviation |

1,422 |

1,372 |

+€50m |

+3.6% |

|

Retail and services |

742 |

706 |

+€36m |

+5.1% |

|

Real estate |

198 |

188 |

+€10m |

+5.2% |

|

International and airport developments |

1,064 |

384 |

+€680m |

- |

|

of which TAV Airports |

893 |

342 |

+€551m |

- |

|

of which AIG |

125 |

- |

- |

- |

|

Other activities |

113 |

177 |

-€64m |

-36.4% |

|

Inter-sector eliminations |

(185) |

(231) |

-€46m |

-19.9% |

Reminder of 2018 assumptions and forecasts, unchanged since the publication of half-year results on 30 July 2018

-

Traffic growth assumption for Paris Aéroport between +2.5% and +3.5% in 2018 compared to 2017.

-

Traffic growth assumption for TAV Airports5: growth above 30% in 2018 compared to 2017;

-

Revision of consolidated EBITDA6 forecast: increase between +17% and +22% in 2018 compared to 2017, with the full-year effect of the full consolidation of TAV Airports and the effect of the full consolidation of AIG since April 2018:

-

2018 consolidated EBITDA excluding the full consolidation of TAV Airports and AIG: increase between +2.5% and +3.5% in 2018 compared to 2017.

-

TAV Airports EBITDA6/7 forecast : increase between +14% and +16% in 2018 compared to 2017.

-

- Maintained pay-out of 60% of NRAG 2018.

Augustin de Romanet, Chairman and CEO of Aéroports de Paris SA-Groupe ADP, stated:

"2018 first 9 months revenue increased by 29.2%, at €3,353 million thanks to the very good traffic dynamics in the whole group. Moreover, the revenue benefitted from the effect of the full consolidation of the results of TAV Airports for 9 months and Airport International Group, concessionary of Queen Alia International Airport in Amman, Jordan, for 6 months. Retail activities' growth in Paris was supported by the dynamism of bars and restaurants and airside shops. Sales per passenger of airside shops was stable, the positive traffic mix being negatively impacted by the strong euro and important works in terminal 2E, halls K and L leading to temporary shops closing during the work. Given these items, all the forecasts of the group for 2018 are confirmed."